How it works, when it makes sense, and when it doesn’t.

Indexed Universal Life Insurance, commonly referred to as an IUL, is a form of permanent life insurance that combines lifelong death benefit protection with tax-advantaged cash value growth linked to market indexes. Indexed universal life insurance is designed to limit downside risk while supporting long-term planning objectives such as retirement income, family protection, and legacy strategies.

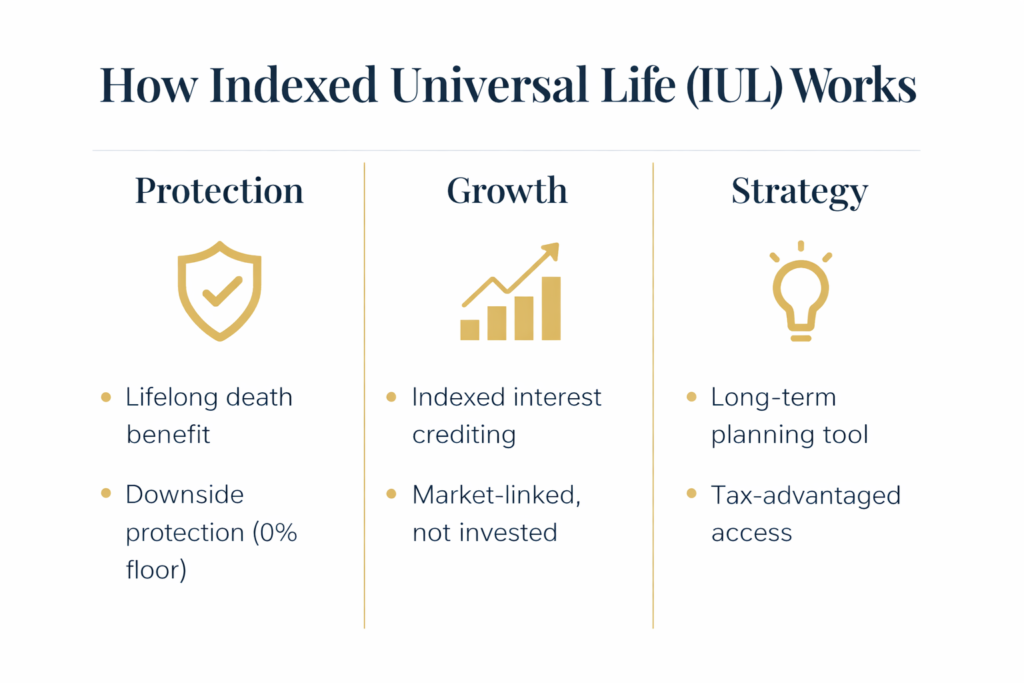

Indexed Universal Life (IUL) combines insurance protection with market-linked growth features and long-term planning flexibility, making policy structure and expectations critical.

Indexed Universal Life (IUL) is a type of permanent life insurance designed to provide lifelong death benefit protection while allowing cash value to grow over time.

Unlike traditional investment accounts, IUL cash value is not directly invested in the stock market. Instead, interest is credited based on the performance of selected market indexes, subject to built-in limits designed to manage risk.

IUL is a long-term financial tool that is typically used as part of a broader strategy — not a standalone investment replacement.

IUL cash value is not directly invested in the stock market. Interest is credited based on the performance of a chosen market index, allowing participation in market gains without direct exposure to market losses.

Most IUL policies include a floor — often 0% — which protects cash value from negative market years. In exchange, growth is typically limited by caps or participation rates during strong market performance.

Two IUL policies can perform very differently based on how they are designed, funded, and managed. Premium structure, cost efficiency, and index allocation all play a significant role in long-term outcomes.

One of the reasons Indexed Universal Life (IUL) is often used in long-term planning is its unique tax treatment under current U.S. tax law. Cash value inside an IUL policy generally grows on a tax-deferred basis, meaning gains are not taxed annually as long as they remain within the policy.

In addition, life insurance death benefits are generally received income-tax free by beneficiaries, and policy distributions may be accessed tax-efficiently when structured and managed properly. However, tax outcomes can vary depending on how a policy is funded, accessed, or surrendered.

For official guidance on how life insurance proceeds and distributions are treated for federal income tax purposes, see the IRS guidance on life insurance proceeds.

• A long-term financial strategy

• Designed for protection and tax efficiency

• Structured to manage downside risk

• Most effective with proper funding and time horizon

• A stock market investment

• A short-term solution

• A guaranteed high-return product

• Appropriate for every situation

IUL is not a replacement for every financial tool, which is why understanding how it compares to other financial planning strategies is important.

Individuals and families may consider IUL as part of their financial planning strategy for reasons such as:

• Supplemental tax-advantaged retirement income

• Long-term family protection

• Legacy and estate planning

• Diversification away from market-only risk

• Access to cash value without traditional retirement account restrictions

• You have a long-term planning horizon

• You value downside protection alongside growth potential

• You are seeking tax-efficient access to capital

• You already contribute to traditional retirement accounts

• You understand the tradeoffs between safety and upside

Many individuals consider IUL after maxing out traditional accounts or exploring insurance-based retirement strategies.

• You need short-term liquidity

• You are uncomfortable with insurance-based strategies

• You are seeking unlimited market upside

• The policy would be underfunded or improperly structured

• You prefer fully guaranteed investment products

Many misconceptions about Indexed Universal Life insurance stem from policies that were poorly designed or misunderstood.

IUL is neither inherently good nor bad — outcomes depend on structure, expectations, and alignment with individual goals. Education and proper planning are essential to determining whether this strategy makes sense in a given situation.

If you’re exploring tax-advantaged growth and lifetime protection, a brief strategy conversation can help determine whether IUL aligns with your goals and time horizon.

If you’re still exploring options, you may want to review our retirement education resources before scheduling a conversation.

Disclaimer:

This content is provided for educational purposes only and does not constitute financial, tax, or legal advice. Insurance products and strategies vary by carrier, policy design, and individual circumstances. Guarantees are backed by the claims-paying ability of the issuing insurance company. Past performance and illustrations are not guarantees of future results.